Our Steady Momentum PutWrite strategy attempts to outperform the CBOE PUT index, which writes cash secured puts on the S&P 500. An investable version of this strategy can be purchased with the ETF PUTW. The historical data for PUT extends back more than 30 years, highlighting how writing puts can be an attractive strategy.

In addition to the S&P 500, CBOE also tracks the same strategy on RUT with their index PUTR. Below is the historical data since 2001.

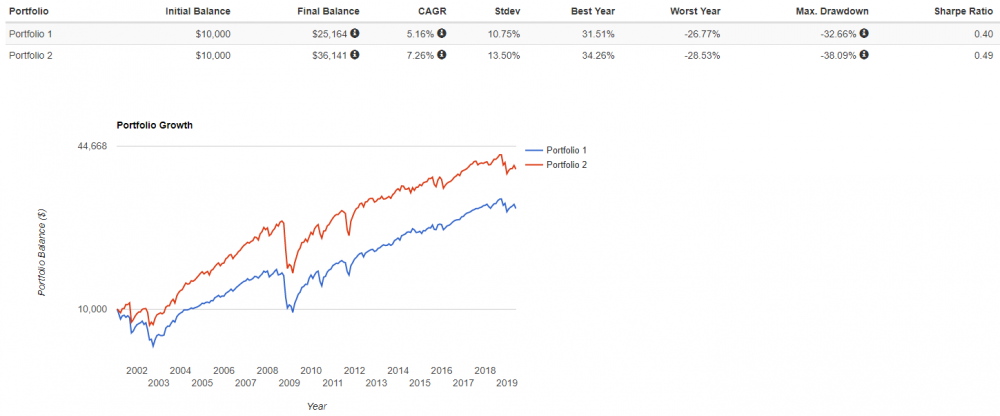

Portfolio 1: PUT

WE RECOMMEND THE VIDEO: Trader Varun Live Trading13 Nov |OLYMP TRADE | OlympTrade 100% winning strategy|1minute strategy|

Hi I welcome you all on my youtube channel. Like | Comment | Share | Subscribe Register in Olymptrade Get 50% welcome Bonus ...

Portfolio 2: PUTR

Past performance doesn't guarantee future results, and shouldn't be relied upon exclusively when making investment decisions.

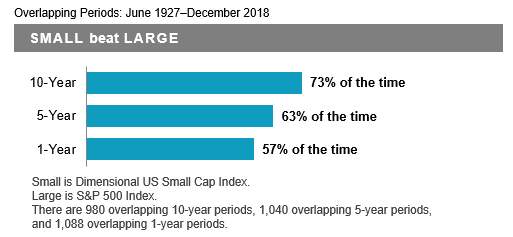

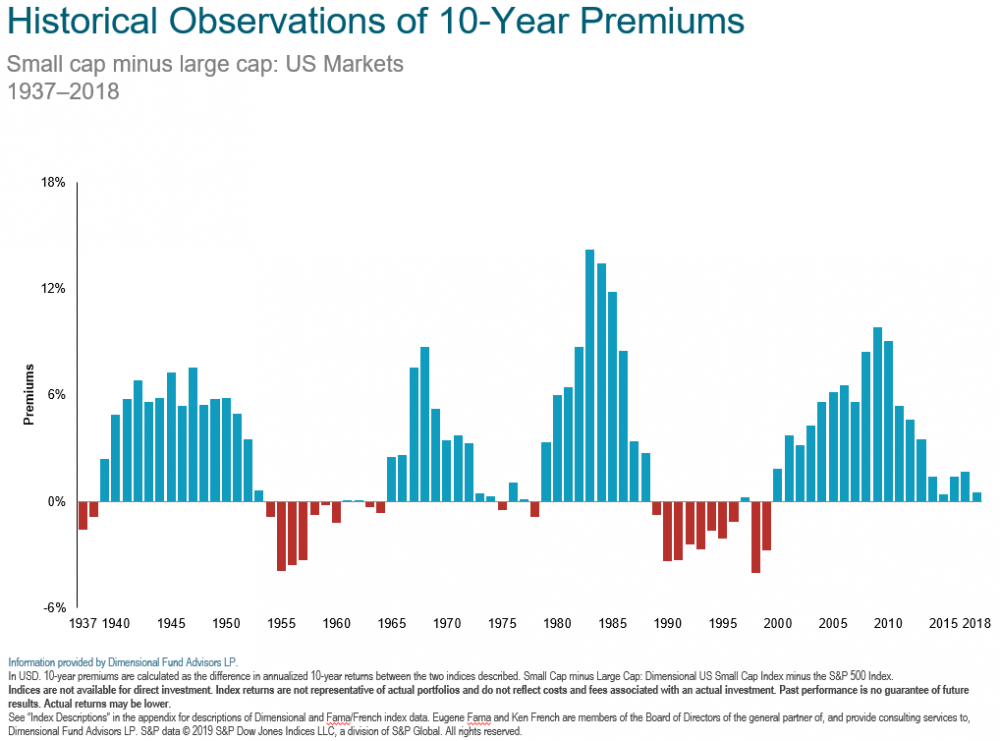

PUTR has beat PUT by 210 bps from 02/2001 - 05/2019, which is largely explained by the fact that IWM beat SPY by 199 bps (7.47% vs. 5.48%). This should not be thought of as random chance, as academic research has found there to be a persistent and pervasive size premium (small outperforms large. see charts below from Dimensional) in the historical data that is intuitive as a risk premium. For example, we can see that PUTR's 40% relative higher return (7.26% vs. 5.16%) came also with 25% higher risk (13.5% vs. 10.75%). Therefore the Sharpe Ratio's are similar. This is what would be expected in a world of highly (although not perfectly) efficient markets. All asset classes are expected to have roughly comparable Sharpe Ratio's over a long period of time, and therefore the best way to increase your expected Sharpe Ratio is with diversification.

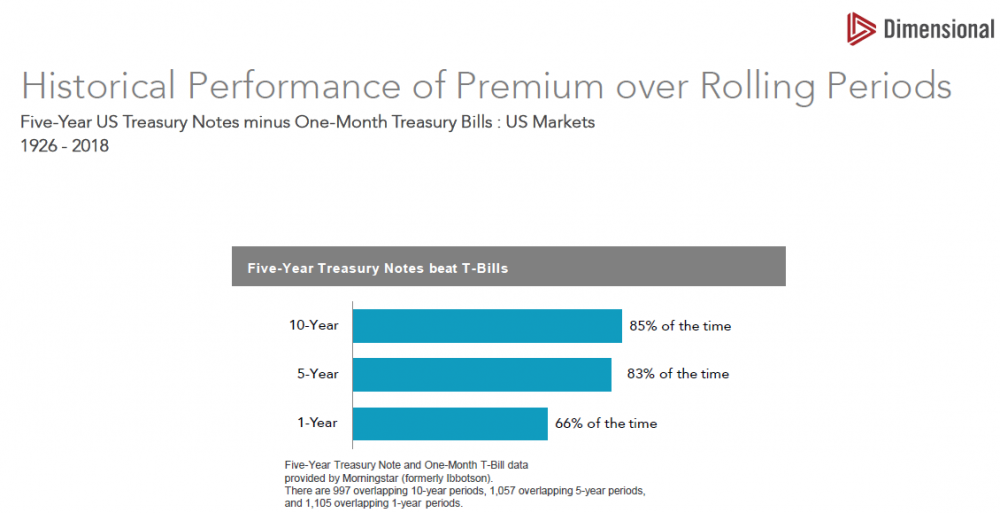

This same thought process of an expected long term risk premium can be applied to our usage of collateral in the form of

5 yr treasuries. I had Dimensional create the following chart, highlighting the persistence of 5 yr treasuries outperforming T-bills since 1926.

I hope readers find this type of scientific data analysis transformational to your way of thinking, as I know I certainly did when I first learned of it. I believe this type of thought process should inform your entire investment portfolio, not just this particular strategy. For example, this same process has also gone into the construction of our ETF portfolio alerts, which are provided to Steady Momentum subscribers at no additional charge.

If you were seeking out advice for a health related issue you were having, wouldn't you rather get that advice from a professional who has spent their career studying peer reviewed scientific research vs. picking up a magazine at the checkout line at the grocery store or asking a friend/family member/co-worker what they think you should do? These sources of advice may be sincere, but the consequences of bad advice are simply too high. If so, shouldn't the same standard apply to your financial planning and investment decisions?

Jesse Blom is a licensed investment advisor and Vice President of Lorintine Capital, LP . He provides investment advice to clients all over the United States and around the world. Jesse has been in financial services since 2008 and is a CERTIFIED FINANCIAL PLANNER™ professional . Working with a CFP® professional represents the highest standard of financial planning advice. Jesse has a Bachelor of Science in Finance from Oral Roberts University. Jesse manages the Steady Momentum service, and regularly incorporates options into client portfolios.

What Is SteadyOptions?

Full Trading Plan

Complete Portfolio Approach

Diversified Options Strategies

Exclusive Community Forum

Steady And Consistent Gains

High Quality Education

Risk Management, Portfolio Size

Performance based on real fills

Non-directional Options Strategies

10-15 trade Ideas Per Month

Targets 5-7% Monthly Net Return

Recent Articles

Articles

Pricing Models and Volatility Problems

Most traders are aware of the volatility-related problem with the best-known option pricing model, Black-Scholes. The assumption under this model is that volatility remains constant over the entire remaining life of the option.

By Michael C. Thomsett, August 16

- Added byMichael C. Thomsett

- August 16

Option Arbitrage Risks

Options traders dealing in arbitrage might not appreciate the forms of risk they face. The typical arbitrage position is found in synthetic long or short stock. In these positions, the combined options act exactly like the underlying. This creates the arbitrage.

By Michael C. Thomsett, August 7

- Added byMichael C. Thomsett

- August 7

Why Haven't You Started Investing Yet?

You are probably aware that investment opportunities are great for building wealth. Whether you opt for stocks and shares, precious metals, forex trading, or something else besides, you could afford yourself financial freedom. But if you haven't dipped your toes into the world of investing yet, we have to ask ourselves why.

By Kim, August 7

- Added byKim

- August 7

Historical Drawdowns for Global Equity Portfolios

Globally diversified equity portfolios typically hold thousands of stocks across dozens of countries. This degree of diversification minimizes the risk of a single company, country, or sector. Because of this diversification, investors should be cautious about confusing temporary declines with permanent loss of capital like with single stocks.

By Jesse, August 6

- Added byJesse

- August 6

Types of Volatility

Are most options traders aware of five different types of volatility? Probably not. Most only deal with two types, historical and implied. All five types (historical, implied, future, forecast and seasonal), deserve some explanation and study.

By Michael C. Thomsett, August 1

- Added byMichael C. Thomsett

- August 1

The Performance Gap Between Large Growth and Small Value Stocks

Academic research suggests there are differences in expected returns among stocks over the long-term. Small companies with low fundamental valuations (Small Cap Value) have higher expected returns than big companies with high valuations (Large Cap Growth).

By Jesse, July 21

- Added byJesse

- July 21

How New Traders Can Use Trade Psychology To Succeed

People have been trying to figure out just what makes humans tick for hundreds of years. In some respects, we’ve come a long way, in others, we’ve barely scratched the surface. Like it or not, many industries take advantage of this knowledge to influence our behaviour and buying patterns.

- Added byKim

- July 21

A Reliable Reversal Signal

Options traders struggle constantly with the quest for reliable reversal signals. Finding these lets you time your entry and exit expertly, if you only know how to interpret the signs and pay attention to the trendlines. One such signal is a combination of modified Bollinger Bands and a crossover signal.

By Michael C. Thomsett, July 20

- Added byMichael C. Thomsett

- July 20

Premium at Risk

Should options traders consider “premium at risk” when entering strategies? Most traders focus on calculated maximum profit or loss and breakeven price levels. But inefficiencies in option behavior, especially when close to expiration, make these basic calculations limited in value, and at times misleading.

By Michael C. Thomsett, July 13

- Added byMichael C. Thomsett

- July 13

Diversified Leveraged Anchor Performance

In our continued efforts to improve the Anchor strategy, in April of this year we began tracking a Diversified Leveraged Anchor strategy, under the theory that, over time, a diversified portfolio performs better than an undiversified portfolio in numerous metrics. Not only does overall performance tend to increase, but volatility and drawdowns tend to decrease: